Blog

How Deferred Compensation Fits Into Your Broader Tax and Retirement Plan

June 3, 2026

Where, When, And How It Becomes More Valuable

Image created using AI by Google Gemini

Key Takeaways

- Deferred compensation is most valuable when it is evaluated as part of a coordinated plan, not in isolation

- During working years, deferred compensation can create planning flexibility that extends beyond simply reducing taxes

- The way deferred compensation is structured during working years can influence income, taxes, and more opportunities across multiple decades in retirement

Deferred compensation is often evaluated on a single dimension: how much income can be deferred today, and at what rate will it be taxed when received? Those are important starting points, but they understate what a well-structured deferred compensation plan can do.

For high earners with access to these plans, deferred compensation can influence the tax picture not just during the deferral years, but throughout retirement. The way deferred compensation interacts with other accounts and income sources is where much of its long-term value is found.

Why Coordination Matters

Most high earners accumulate retirement assets across several different types of accounts, each with its own tax treatment:

- Pre-tax (tax-deferred): Traditional 401(k)s, Traditional IRAs, and deferred compensation plans. Contributions reduce taxable income today, but withdrawals are taxed as ordinary income in the future.

- After-tax (tax-free): Roth 401(k)s and Roth IRAs. Contributions are made with after-tax dollars, but qualified withdrawals, including growth, are tax-free.

- Taxable accounts: Individual and Joint accounts and other non-retirement investments. These offer flexibility but no upfront tax deduction, and growth is subject to capital gains taxes.

A common challenge for high earners is that many of their retirement assets end up concentrated in pre-tax accounts. That concentration creates a predictable challenge: a larger portion of future retirement income becomes taxable, often at times when the retiree has limited flexibility to control it, such as when they must begin taking their required minimum distributions. Deferred compensation can either add to that problem or help manage it, depending on how it is used. The difference comes down to how well the deferred compensation strategy is coordinated with the rest of the plan.

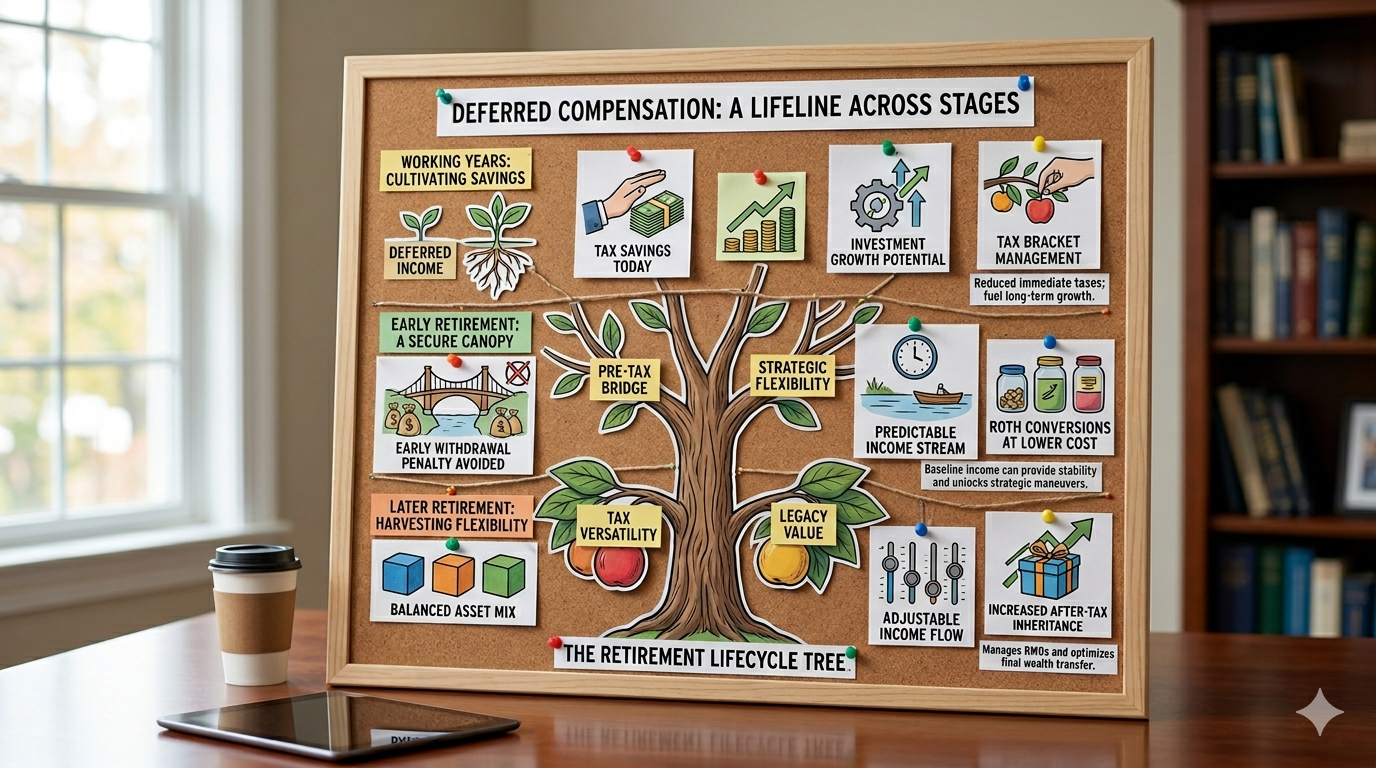

What Deferred Compensation Does During Working Years

The most immediate effect of deferring income is a reduction in current taxable income. That opportunity alone can be meaningful, but the more important impact is what that reduction makes possible.

Lower taxable income can create flexibility around decisions that are otherwise constrained at higher income levels. That flexibility could mean staying below thresholds that trigger additional taxes or phaseouts, or it may create room to recognize income on your own terms, rather than being forced into it at higher rates.

This is particularly relevant when it comes to building tax-free assets. High earners are often limited in their ability to contribute to Roth accounts or complete Roth conversions efficiently. By reducing taxable income through deferred compensation, it may create the opportunity to shift dollars into Roth accounts at a lower effective tax cost than would otherwise be available. Over time, that can meaningfully change the composition of a balance sheet that might otherwise be heavily skewed toward pre-tax assets.

What Deferred Compensation Does in Early Retirement

For those who retire early, they need to determine how they will continue to fund their lifestyle. Many early retirees look to their pre-tax retirement accounts like IRAs and 401(k)s to bridge that income gap— however, distributions taken from these accounts before age 59½ trigger a 10% early withdrawal penalty. One way to bridge that gap without triggering any unnecessary penalties is by using deferred compensation payments to partly or entirely reduce their reliance on their pre-tax accounts.

A second benefit during this phase of retirement is because distributions are scheduled in advance, deferred compensation payments create a baseline level of predictable income. That predictability reduces the need to generate cash flow from investment accounts based on market conditions or short-term needs, allowing the investment portfolio to remain more fully invested during a period when long-term growth still matters. When income planning begins with a known starting point, other planning strategies can be layered on more intentionally.

These other strategies may include realizing capital gains at favorable rates, completing Roth conversions in a controlled manner, or coordinating the timing of other income sources like Social Security. The goal is not simply to fill a gap, but to use a period of relatively low and flexible income to make decisions that improve long-term tax efficiency.

What Deferred Compensation Does in Later Retirement

As retirement progresses, flexibility tends to decline. Social Security benefits begin, and required minimum distributions (RMDs) eventually force income out of pre-tax accounts whether it is needed or not. At this stage, earlier deferred compensation decisions begin to have a more lasting impact.

The way income was deferred and distributed in earlier years influences how large pre-tax account balances become later in retirement, and therefore how significant RMDs will be. Larger balances generally lead to higher RMDs and therefore more persistent taxable income, which may push retirees into higher tax brackets or even increase Medicare premiums.

By contrast, a more coordinated approach can result in a more balanced mix of assets across pre-tax, Roth, and taxable accounts. That balance provides more versatility in managing income, allowing retirees to adjust withdrawals in response to changing needs, tax laws, or market conditions.

There is also a longer-term consideration around how assets are passed on to beneficiaries. Large pre-tax balances can create a tax burden for heirs, particularly under current distribution rules. A more balanced asset mix may improve the after-tax value of what is ultimately transferred downstream, especially with larger Roth account balances.

Deferred compensation itself does not solve these issues, but the way it is used can meaningfully influence how they play out.

Putting It All Together

When deferred compensation is integrated into a broader plan, its impact can be felt across multiple phases of life:

- During peak earning years: Deferred compensation can expand available cashflow and tax planning opportunities by reshaping taxable income during these years

- In early retirement: Deferred compensation distributions in these years can define a more controlled and deliberate income environment, while also avoiding unnecessary early withdrawal penalties from pre-tax accounts

- In later retirement: Decisions made about deferred compensation in earlier years can lead to greater flexibility in these years as income becomes more constrained due to RMDs, Social Security, and other factors that come into play

None of this happens automatically, and the right approach will depend heavily on an individual’s income, account balances, retirement timeline, and overall financial goals. But for high earners who have access to deferred compensation and are thinking about retirement strategically, the coordination opportunities across these phases of life are significant.

Summary

Deferred compensation is most powerful not as a standalone strategy, but as part of a coordinated approach to managing income and taxes over time. When used thoughtfully, it can influence not just when income is taxed, but how financial decisions are made across every stage of retirement.

Good financial planning isn’t a “one size fits all” experience. If you’re thinking about how this applies to your own situation, you’re already at the point where having a conversation makes sense. That’s where partnering with our practice begins:

This post was researched and written by the author with the assistance of AI writing tools. All content reflects the author’s own views, has been independently verified, and has been reviewed and approved prior to publication.