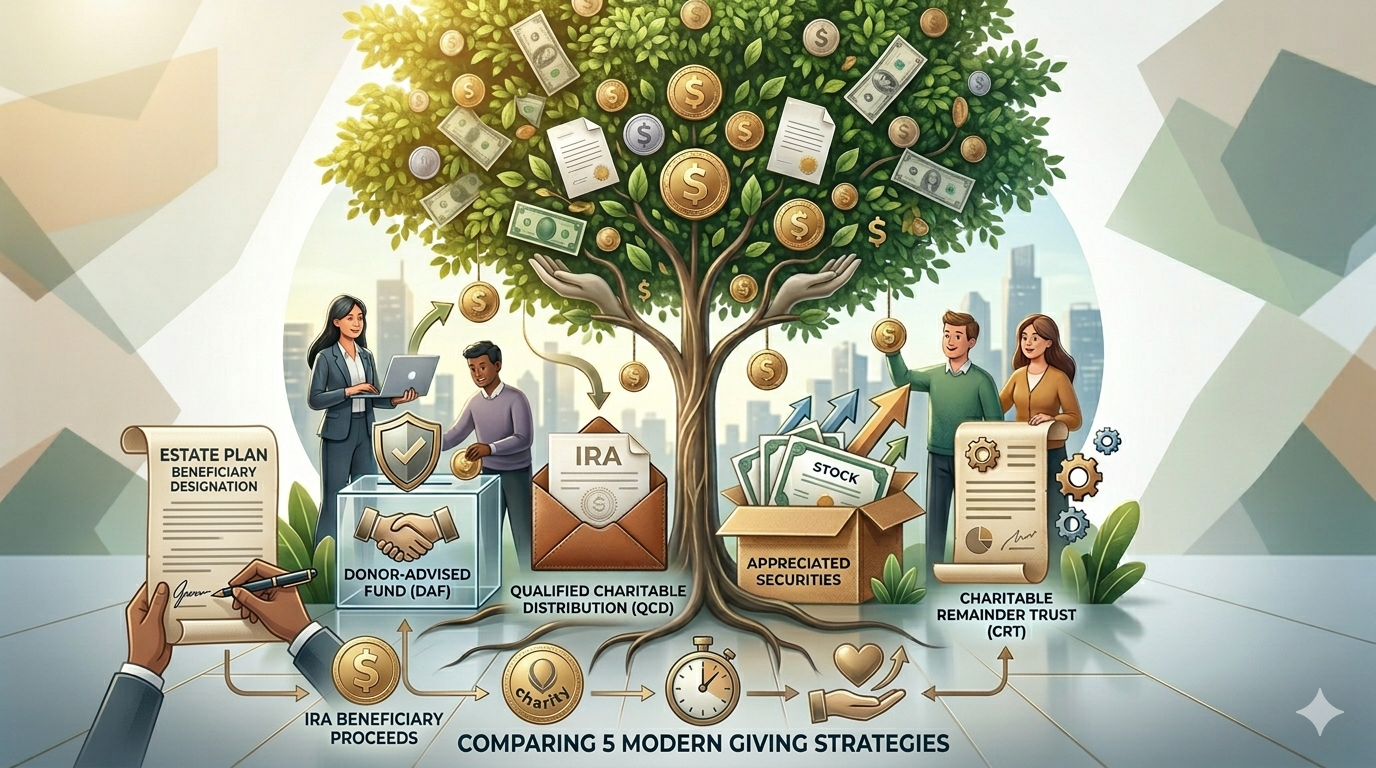

Tax-Efficient Ways to Give More and Pay Less

Image created using AI by Google Gemini

Key Takeaways

- Charitable giving can be structured to reduce taxes today while supporting long-term impact

- Different vehicles, from QCDs to DAFs to CRTs, offer varying levels of tax efficiency, flexibility, and complexity

- For high earners and retirees, thoughtful charitable planning is an extension of broader tax strategy, not just philanthropy for the sake of being generous

Many people think about charitable giving as a simple decision: how much to give and where to give it. But from a tax planning perspective, how you give can matter just as much as how much you give.

The right structure can reduce taxable income, defer or eliminate capital gains, and in some cases generate an income stream, all while supporting the causes you care about. Below is a look at some common charitable giving strategies and what makes each one worth understanding.

Qualified Charitable Distributions (QCDs)

What it is: A direct transfer from an IRA to a qualified charity, available to individuals age 70½ or older.

- A QCD accomplishes something most charitable strategies cannot: it satisfies your required minimum distribution (RMD) while keeping the distribution entirely out of your taxable income. For retirees who don’t need to use their RMDs for living expenses and want to give to charity anyways, this is often the most efficient and least complicated option available.

Eligibility: Must be age 70½ or older. In 2026, the annual limit is $111,000 per individual. Funds must come from an IRA (not an active 401(k)) and cannot be directed into a Donor Advised Fund (DAF).

Tax benefits: Because the distribution is excluded from taxable income, a QCD can lower your AGI, which may reduce your marginal tax rate, Medicare premiums, and the portion of Social Security subject to taxes. It should be noted that a QCD can only reduce AGI when the donor is already subject to RMDs. For people who are older than age 70.5 but younger than when their RMDs begin at age 73 or 75, their QCDs would not reduce AGI until after their RMDs begin.

Tradeoffs: Funds must go directly to charity in the year of distribution. You also cannot take a separate charitable deduction for the same gift, as the tax benefit already comes from not being counted in taxable income.

Donating Appreciated Stock Instead of Cash

What it is: Transferring long-term appreciated securities directly to a charity rather than selling them first and donating the cash proceeds.

- If you donate cash to charity and funded that gift by selling appreciated investments, you paid capital gains tax unnecessarily. Donating the shares directly sidesteps the tax entirely.

Eligibility: No formal requirements to enact the strategy, although the asset must have been owned longer than one year to qualify for a deduction at full fair market value. The gifting of appreciated shares can go into a Donor Advised Fund as well. However, the donor must be itemizing to receive the deduction, and the donation must be greater than 0.5% of the donor’s AGI to qualify for any deduction. For donors who take the standard deduction, the opportunity to deduct up to $1,000 (single) or $2,000 (married filing jointly) only applies to gifts made with cash, not appreciated stock, and it also does not apply when any kind of donation is gifted directly into a Donor Advised Fund.

Tax benefits: You avoid capital gains tax on the appreciation and receive a deduction for the full fair market value of the shares, which is a meaningful advantage compared to the sell-then-donate-cash approach.

Tradeoffs: Requires a direct share transfer rather than a cash gift, along with proper documentation. Most major brokerages and charities handle this routinely though.

Donor Advised Funds (DAFs)

What it is: A charitable investment account that lets you contribute assets, receive an immediate tax deduction if you itemize and donate more than 0.5% of your AGI, and distribute grants to charities over time on your own schedule.

- A DAF can let you separate the timing of your tax deduction from the timing of your giving. You can contribute in a high-income year to capture the deduction, then recommend grants to your chosen charities over the next several years.

Eligibility: Available to most taxpayers. Deduction limits depend on your income and the type of asset contributed.

Tax benefits: You receive a deduction in the year of contribution, assets grow tax-free inside the account, and you can contribute appreciated securities without triggering capital gains taxes.

Tradeoffs: Contributions to a DAF are irrevocable, as the funds are permanently committed to charitable use. Grants are formally made by the sponsoring organization based on your recommendations, though in practice sponsors follow donor intent closely.

Naming Charities as IRA Beneficiaries

What it is: Designating a qualified charity as a full or partial beneficiary of an IRA or other tax-deferred retirement account.

- This is one of the simplest charitable strategies available. It requires no trust to be established, no special account to be created, and no annual action. Yet it’s frequently overlooked, and the tax efficiency is significant.

Eligibility: No formal requirements.

Tax benefits: Charities are tax-exempt, meaning the full account value transfers to the organization without being reduced by income taxes. Non-spousal heirs who inherit the same account don’t have that advantage, as they must fully withdraw the funds within 10 years and pay ordinary income tax on every distribution. Leaving pre-tax retirement assets to charity and other assets, like Roth accounts or taxable investments, to heirs is often the most tax-efficient way to structure an estate with philanthropic aspirations.

Tradeoffs: Reduces the inheritance available to heirs, though it can be paired with other strategies —such as Roth conversions or life insurance— to balance charitable and family legacy goals.

Charitable Remainder Trusts (CRTs)

What it is: An irrevocable trust that pays income to you or other named beneficiaries for a set period —either a term of years or your lifetime— with the remaining assets passing to charity at the end.

- CRTs are the most complex strategy on this list, but they serve a specific purpose well: converting highly appreciated assets into a diversified income stream without triggering an immediate tax bill.

Eligibility: No formal requirements, but CRTs are best suited for higher-net-worth individuals with highly appreciated assets and a committed long-term charitable intent. Legal and administrative costs make them less practical for smaller gift amounts.

Tax benefits: You receive a partial upfront charitable deduction based on the estimated present value of what the charity will eventually receive. You avoid an immediate capital gains tax on contributed assets. The trust sells the appreciated property tax-free and reinvests the full proceeds, with gains flowing to you gradually over time. The contributed assets are also removed from your taxable estate.

Tradeoffs: CRTs involve meaningful legal complexity and upfront cost to establish, and like all the strategies listed here, contributions are irrevocable.

Summary

| Strategy | How it works | Who it is best for | Timing | Key tax benefits | Main tradeoffs |

| Qualified Charitable Distribution (QCD) | Direct IRA transfer to charity; counts toward your RMD | Age 70½+ | During life | Excluded from taxable income; lowers AGI for those already taking their RMDs and may reduce Medicare premiums and amount of Social Security subject to taxation | Must go directly to charity in the same year and cannot be donated into a DAF; cannot also itemize the gift as a deduction |

| Donate Appreciated Stock | Transfer appreciated securities directly to charity instead of selling first | Primarily taxpayers who itemize their deductions and plan to donate more than 0.5% of their AGI | During life | Avoids capital gains tax; deductible at fair market value if itemizing, but only to the extent contributions exceed 0.5% of AGI | No deduction for non-itemizers; deduction reduced by 0.5% AGI floor; requires direct share transfer and proper documentation |

| Donor Advised Fund (DAF) | Contribute assets now, recommend grants to charities over time | Primarily taxpayers who itemize their deductions and plan to donate more than 0.5% of their AGI | During life | Immediate deduction if itemizing (subject to 0.5% AGI floor); tax-free growth; avoids capital gains on appreciated assets | No deduction for non-itemizers (except limited cash gifts); deduction reduced by 0.5% AGI floor; contributions are irrevocable and grants are controlled by sponsoring organization |

| IRA Beneficiary Designation | Name a charity as full or partial IRA beneficiary | Most taxpayers | At death | Charity receives full account value tax-free; avoids income tax burden that heirs would otherwise face | Reduces inheritance to heirs; can be paired with Roth accounts or life insurance to compensate |

| Charitable Remainder Trust (CRT) | Irrevocable trust pays income to you for a set term; remainder goes to charity | Higher net worth families; highly appreciated assets | Both during life and at death | Partial upfront deduction; deferred capital gains; income stream; assets removed from taxable estate | Legal complexity and cost to establish; contributions are irrevocable |

Tax-efficient charitable giving isn’t about changing your generosity; it’s about making sure that generosity is also working as hard as possible on your tax return. When coordinated properly, these strategies can reduce lifetime tax liability while increasing the impact of every dollar you give.

Good financial planning isn’t a “one size fits all” experience. If you’re thinking about how this applies to your own situation, you’re already at the point where having a conversation makes sense. That’s where partnering with our practice begins:

Clearfront Advisory does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

This post was researched and written by the author with the assistance of AI writing tools. All content reflects the author’s own views, has been independently verified, and has been reviewed and approved prior to publication.