Blog

Summer School 301: The Tax Loss Harvesting Playbook

June 10, 2026

From Basics to Advanced Strategies

By Kevin Curley II, CFP®, CEPA® | Senior Wealth Advisor, Clearfront Advisory

Introduction

Welcome to Summer School — a financial education series for people who are financially successful but haven’t spent their careers studying investment vehicles and planning tools. No jargon without explanation. No condescension. Just the information you need to make

better financial decisions.

This post covers one of the most useful and most misunderstood tools in taxable investing: tax loss harvesting. It spans from something an individual investor can do in a brokerage account to far more complex institutional strategies now drawing industry attention. We will walk through each level so you understand what is happening, why it can work, and what tradeoffs come with it.

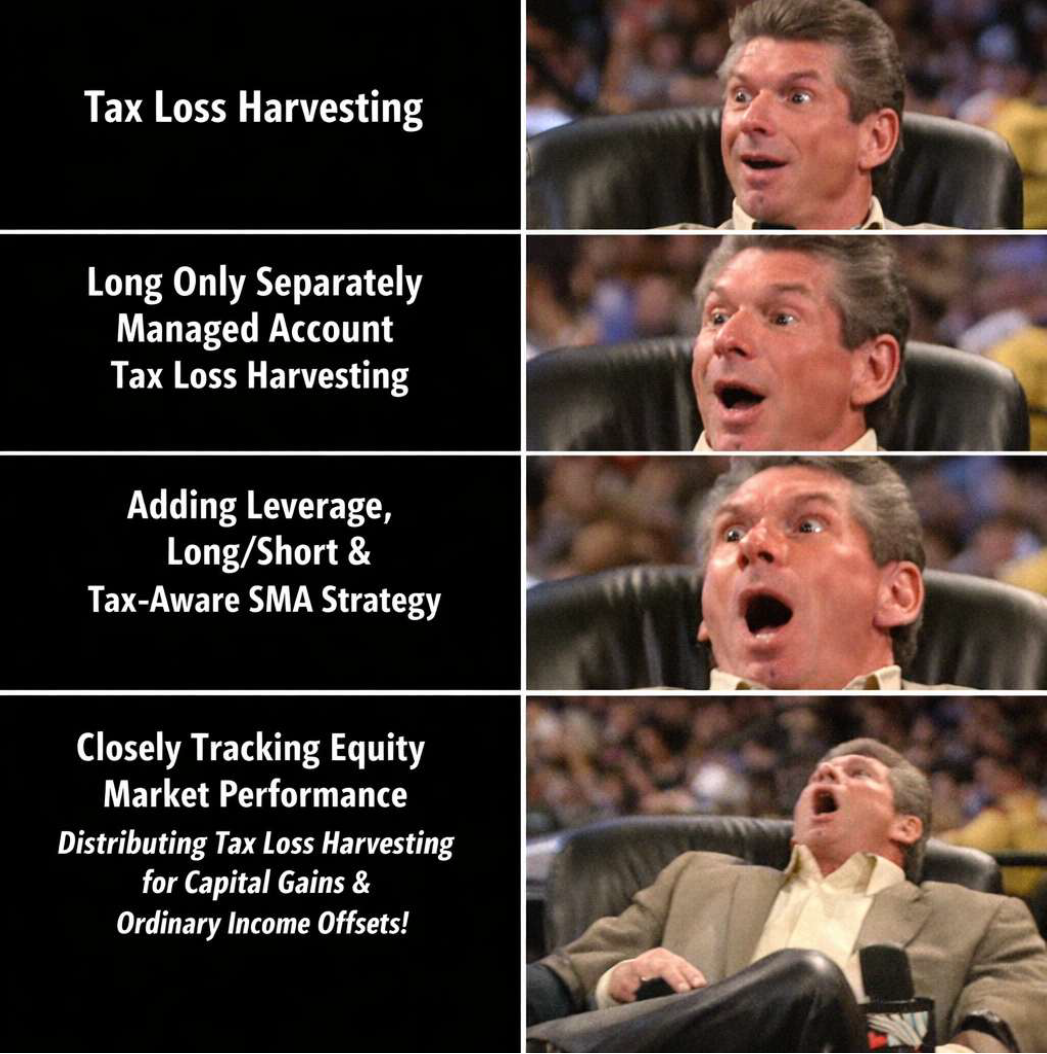

Tax Loss Harvesting 101: The Basics

What It Is:

Tax loss harvesting is the practice of selling an investment that has lost value in order to capture that loss for tax purposes, then reinvesting the proceeds in a similar but not identical investment to maintain your market exposure. That last step matters. The point is not to step out of the market or try to time it. The point is to stay invested while potentially improving the after-tax result.

The mechanics are straightforward. You own a stock or fund that is down $20,000 from your purchase price. You sell it, locking in that $20,000 loss. You use that loss first to offset realized capital gains elsewhere in your portfolio. There is no dollar cap on how much

realized capital losses can offset realized capital gains in a given year. If losses exceed gains, up to $3,000 of net losses can be used to offset ordinary income each year ($1,500 if married filing separately), and any remainder carries forward indefinitely to future tax years.

The aim is to keep similar market exposure while reducing the current tax bill, though returns can differ because the replacement investment is not identical.

The Wash-Sale Rule – The One Rule You Cannot Ignore:

The wash-sale rule prohibits you from claiming a loss if you buy the same or a substantially identical security within 30 days before or after the sale. The window is 61 days total: 30 days before, the day of the sale, and 30 days after. If you sell a fund at a loss on Monday and buy the same fund back on Tuesday, the IRS disallows the loss. You have not harvested anything. You have just traded.

The workaround is to buy a similar but not identical replacement. Sell a large-cap U.S. equity ETF at a loss, then buy a different large-cap U.S. equity ETF that tracks a different index or uses a different construction. You maintain similar exposure while avoiding a straightforward wash sale.

What This Accomplishes:

At the 101 level, tax loss harvesting is mainly a way to offset realized capital gains. If you sold real estate, exercised stock options, or trimmed a concentrated position and created a large capital gain, harvested losses in your portfolio can reduce the taxable amount. For an investor subject to the 23.8% federal rate on long-term gains, every $100,000 in harvested losses can defer roughly $23,800 of federal tax, before state tax effects.

This is not tax elimination. It is usually tax deferral. When you eventually sell the replacement investment, your cost basis will generally be lower than it would have been otherwise, which can increase future taxable gain. The benefit is the time value of money:

you keep that tax payment invested for longer before it comes due.

Tax Loss Harvesting 201: The Long-Only Separately Managed Account

The next evolution beyond individual tax loss harvesting is the separately managed account, or SMA, especially the tax-aware long-only version often used in direct indexing.

Here is how it works. Instead of buying a single ETF for broad market exposure, you own many of the underlying stocks directly in your own account. Because you own the individual securities rather than a fund, you can sell specific losing positions throughout the year, harvest those losses, and replace them with other holdings that keep the portfolio

close to its target exposure.

The Advantages Over The 101 Approach:

- First, scale. A diversified portfolio of individual stocks creates more potential harvesting opportunities than a single fund position. In a volatile year, losses may be available in individual names even if the overall market is up.

- Second, customization. You can exclude individual stocks you already own elsewhere (avoiding concentration), tilt toward factors like dividends or quality, and screen out sectors or companies based on your preferences.

- Third, legacy positions. If you transfer in appreciated stock, the SMA can manage around it, integrating your existing low-basis holdings into the portfolio without triggering an immediate taxable event.

The limitation of the long-only SMA is that it is ultimately constrained by the market. If prices broadly rise, harvesting opportunities shrink. You are working with the natural losses that occur within a rising market — which exist, but are not engineered. The strategy is reactive, not generative.

Tax Loss Harvesting 301: Tax-Aware Long/Short Structures

This is where the strategy becomes far more complex. Recent reporting has highlighted rising investor interest in tax-aware long/short structures.

The basic idea is different from long-only harvesting. A long-only portfolio can only harvest a loss when a position declines. A long/short structure may create more opportunities to realize losses because losses can arise from both long positions that fall and short

positions that rise. Used carefully, that can increase the frequency of realized losses relative to a traditional long-only portfolio.

The goal of these structures is often to stay relatively close to a broad equity benchmark while also realizing more losses than a traditional long-only approach. But the tax mechanics are more technical, the implementation is more complex, and the risks are higher.

Some newer structures are designed to produce tax attributes that may be more valuable than capital losses alone, but the treatment is highly technical, product-specific, and dependent on the investor’s facts and tax reporting. That is not a detail to gloss over.

These strategies can have many positions realizing gains and losses throughout the year. Depending on the structure, some of the realized tax attributes may flow through to investors in a way that can affect their outside tax picture. But that does not make the outcome simple or automatic.

In some cases, tax liability may be deferred for a long time while the position is held. Under current law, assets held until death may receive a step-up in basis, which can reduce or eliminate built-in capital gains, but estate and tax outcomes depend on the specific facts.

Why This Matters

Business owners and highly compensated investors often face tax situations that are lumpy rather than smooth. A business sale, option exercise, concentrated stock sale, or unusually high-income year can create a tax bill large enough to change how the whole portfolio should be managed.

Even if you never use an advanced long/short structure, understanding the spectrum helps you ask better questions. Are your taxable accounts being managed with tax awareness? Are gains and losses being viewed alongside future liquidity events? Are you coordinating portfolio decisions with the tax return, or only reacting after the year is over?

That is the practical value here. Not every investor needs complexity. But most taxable investors are better served when taxes are treated as part of the investment process rather than an afterthought.

One note on risk: these strategies carry complexity that the 101 approach does not. Leverage amplifies both gains and losses. The tax treatment may draw more scrutiny. Minimum investments can also be high. These are not default solutions. They are narrow tools for narrow situations.

There are also simpler but still important tradeoffs that apply even at the 101 and 201 levels. Replacement securities may not perform exactly like what you sold, which introduces tracking error. Harvesting lowers the cost basis of the replacement position, which can increase future taxable gains when you eventually sell. Frequent trading around dividend dates can also affect whether dividends remain qualified for favorable tax treatment. And because state tax treatment is not uniform, the net benefit can vary depending on where you file. This is why tax loss harvesting should be coordinated with the broader portfolio and reviewed with a tax professional rather than treated like a standalone trick.

Key Takeaways

- Tax loss harvesting means selling an investment at a loss to offset realized gains and, within annual limits, some ordinary income.

- The wash-sale rule is the main constraint. You generally need a similar replacement, not the same security.

- Long-only separately managed accounts and direct indexing expand harvesting opportunities by working at the individual security level rather than the fund level.

- More advanced long/short structures may create additional tax opportunities, but they are much more complex and not appropriate for most investors.

- Tax deferral is not the same as tax elimination, and the future outcome depends on holding period, basis, tax law, and the investor’s broader plan.

Sources

- Internal Revenue Code Section 1091.

- IRS Publication 550: Investment Income and Expenses. Internal Revenue Service.

- Pollard, Amelia and Joshua Franklin. “Hedge fund tax craze takes over Wall Street.” Financial Times, April 20, 2026.

- Vanguard. “Maximize your tax savings with tax-loss harvesting.” Investor Resources & Education, 2026.

This post was researched and written by the author with the assistance of AI writing tools. All content reflects the author’s own views, has been independently verified, and has been reviewed and approved prior to publication.

This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Investments are subject to risk, including the loss of principal. Some investments are not suitable for all investors, and there is no guarantee that any investing goal will be met. Diversification does not assure a profit or protect against loss in declining markets, and diversification cannot guarantee that any objective or goal will be achieved. Investing in alternative investments may not be suitable for all investors and involves special risks, such as risk associated with leveraging the investment, utilizing complex financial derivatives, adverse market forces, regulatory and tax code changes, and illiquidity. Past performance is no guarantee of future results. Talk to your financial advisor before making any investing decisions.